Sleep Apnea Dental Appliance Covered by Insurance

Learn how to get a sleep apnea dental appliance covered by insurance at our Fair Lawn practice. We handle the claims process for you in 2026. Schedule today!

Learn how to get a sleep apnea dental appliance covered by insurance at our Fair Lawn practice. We handle the claims process for you in 2026. Schedule today!

You wake up tired, even after a full night in bed. Your partner says you snore, stop breathing, or toss around. Maybe you already tried CPAP and couldn't get used to the mask, tubing, or noise. Then you hear there may be another option, a custom oral appliance from a dental office, and your next question is immediate: will insurance help pay for it?

That question matters in Fair Lawn, Ridgewood, and Glen Rock because sleep apnea treatment isn't just about comfort. It's about getting care you can realistically move forward with. Insurance rules can feel more complicated than the treatment itself, especially when a device is made by a dentist but billed through medical coverage.

A sleep apnea dental appliance covered by insurance is possible for many patients, but the process has to be handled correctly from the start. The diagnosis, sleep study, prescription, provider credentials, and claim submission all need to line up. When they do, the path becomes much more manageable.

Many patients start in the same place. They're exhausted, they know something is wrong with their sleep, and they're frustrated that the solution they've heard about may sound expensive. A custom oral appliance can feel like a relief after struggling with CPAP, but cost anxiety shows up fast.

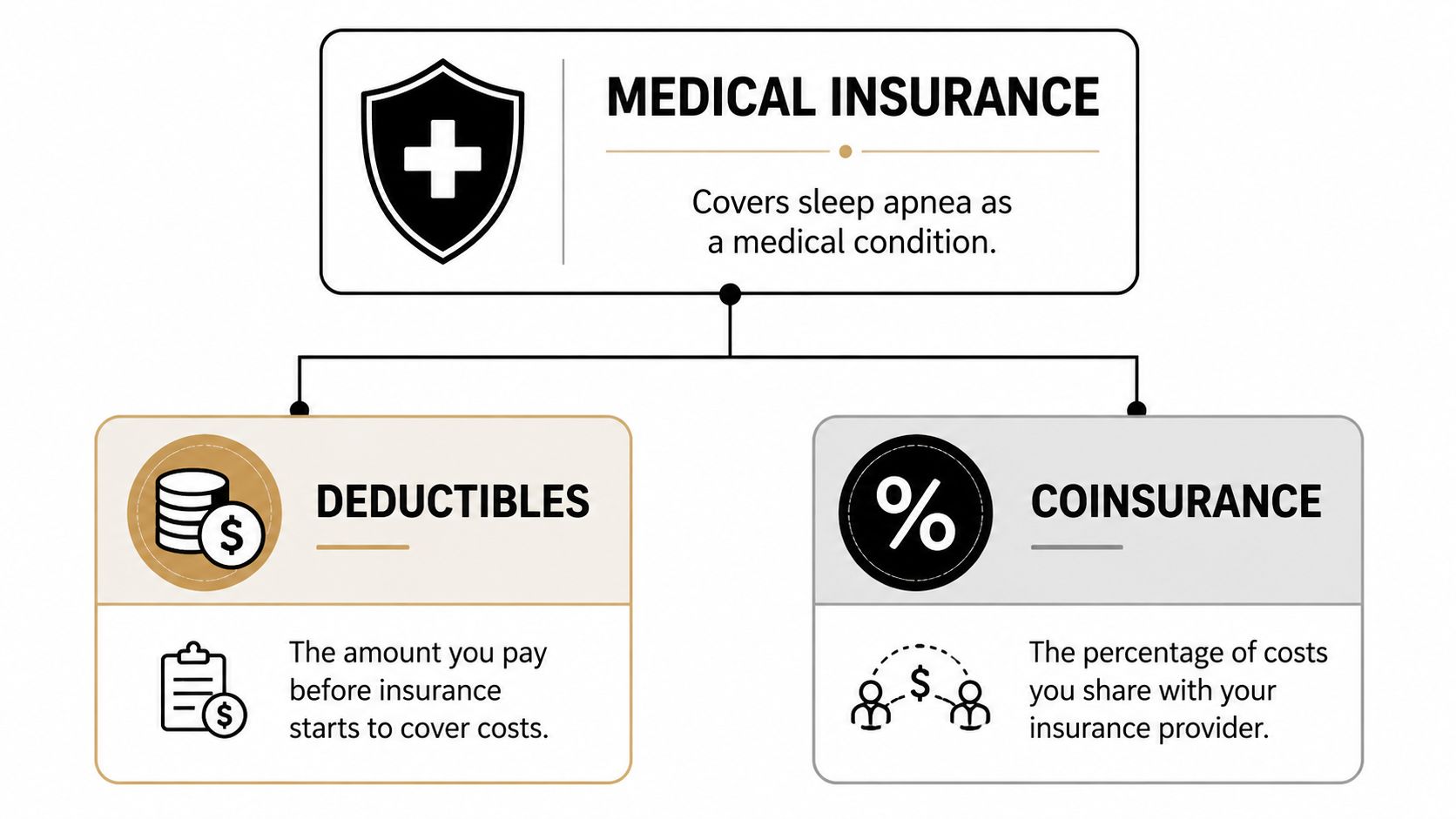

The good news is that oral appliance therapy is often treated as a medical benefit, not a cosmetic or elective dental service. That distinction changes everything. It means the device may qualify under the same general insurance category as other medically necessary equipment used to treat obstructive sleep apnea.

The appliance sits in your mouth, so many people assume dental insurance should cover it. In practice, that's usually where the confusion starts. Sleep apnea is a medical condition, and insurance carriers usually want the claim handled through the medical side of your plan.

Patients also run into a second issue. A dental office can't create coverage out of thin air. The insurer wants proof that the appliance is medically necessary and properly prescribed. If that documentation isn't gathered early, delays follow.

Most insurance problems with sleep apnea appliances don't start at the fitting visit. They start with missing diagnosis details, missing records, or sending the claim to the wrong benefit category.

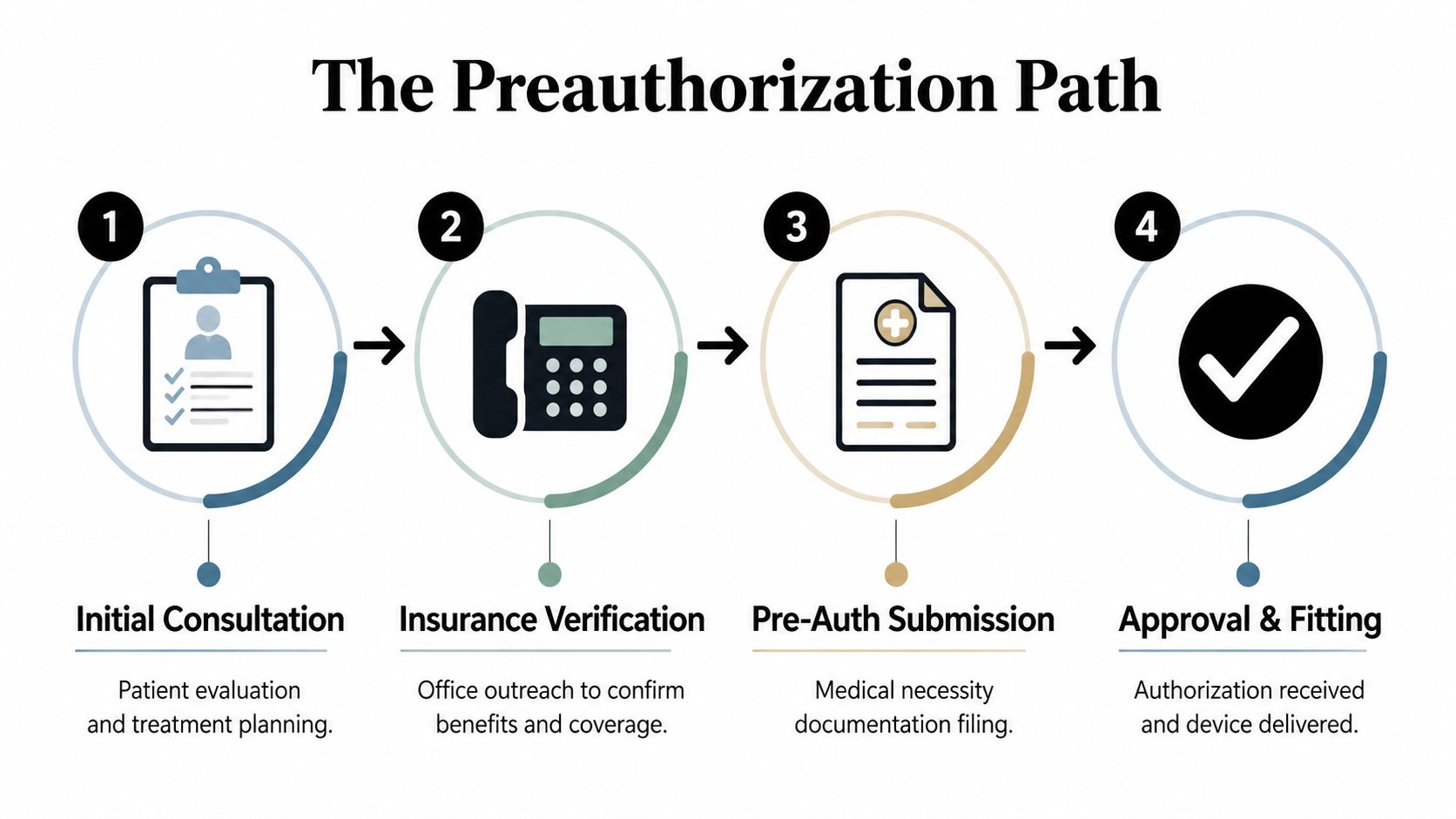

The process becomes easier when you break it into stages:

If you're searching for a dentist in Fair Lawn, NJ who treats sleep-related issues, or even typing in terms like dentist near me because you're trying to solve snoring and sleep apnea, clarity matters as much as treatment. Patients deserve to know what works, what slows claims down, and what questions to ask before committing to care.

A custom sleep apnea appliance is not the same thing as a generic boil-and-bite mouthpiece or an over-the-counter snore guard. The covered version is a custom-made mandibular advancement device, often called a MAD. It is prescribed through the medical pathway for obstructive sleep apnea and made specifically for the individual patient.

The appliance gently repositions the lower jaw during sleep. That forward positioning helps support the airway so it stays more open. This is why insurers don't treat a custom oral appliance like a routine dental accessory. They treat it as therapy for a diagnosed breathing disorder.

According to Reimels Dentistry's overview of insurance-covered sleep apnea oral appliances, custom-made mandibular advancement devices are prescribed by a sleep physician and fabricated from dental impressions to widen the retrolingual space by advancing the hyoid bone, reducing AHI by 50 to 70% in clinical trials and showing 68% patient adherence at one year, compared with 40% for CPAP.

That last point matters in practice. A treatment only helps if a patient can use it. Some patients do very well with CPAP. Others do not tolerate it, and that's where an oral appliance often becomes a practical option.

For patients comparing CPAP alternatives for OSA therapy, it helps to understand that oral appliance therapy isn't a lesser backup. For the right patient, it's a recognized treatment with its own medical standards and follow-up requirements.

Insurance carriers generally want a patient-specific device. That means impressions or digital records are used to create something custom-fitted to your bite and anatomy. A store-bought snoring mouthpiece usually doesn't meet the same standard for coverage.

That's also why many offices use digital workflows instead of old-style methods whenever possible. If you'd like a plain-language explanation of non-CPAP treatment paths, this overview on how to treat sleep apnea without CPAP is a helpful starting point.

Practical rule: If the device wasn't prescribed as treatment for diagnosed obstructive sleep apnea, insurers are far less likely to view it as a covered medical appliance.

Yes, in many cases medical insurance may cover it. The key word is medical. Even though a dentist fits the appliance, carriers usually review it under your health plan because the condition being treated is obstructive sleep apnea.

Claims sent to dental insurance are commonly denied because the appliance is not being used to fix a routine dental problem. It's being used to manage a medically documented airway disorder. That's why insurers often classify it as durable medical equipment, or DME.

This insurance billing review from Nierman Practice Management notes that since Medicare approved oral appliances for obstructive sleep apnea in 2011, most major commercial health plans have followed by categorizing custom appliances as DME, and as of 2026 CMS confirmed these devices remain under the Medicare DME benefit, with beneficiaries typically paying 20% coinsurance after meeting the Part B deductible.

That Medicare history matters because it helped normalize oral appliance coverage across the insurance market. Patients often assume this type of treatment is fringe or self-pay only. It isn't.

A simple breakdown helps:

When you call your insurer, don't ask only, "Do you cover mouthguards?" Ask whether your plan covers a custom oral appliance for obstructive sleep apnea under medical benefits. That wording gets you closer to the accurate answer.

This short video gives a useful overview of how insurance and oral appliance therapy are commonly discussed in practice.

If you're trying to understand how DME benefits work in everyday language, the Affinity Home Medical blog can also help you get familiar with the terms insurers use when discussing equipment coverage.

A patient can have strong medical need and still get a denial if the claim goes through the wrong insurance channel.

A Fair Lawn patient will often do the hardest part first. Get tested, meet with a sleep physician, decide to treat the apnea. Then the insurance review stalls because one report is missing or the prescription language is too vague.

That part is frustrating, but it is fixable.

At Dental Professionals of Fair Lawn, we tell patients the same thing early. Approval usually depends on whether the file shows a clear medical diagnosis, a valid basis for treatment, and records that match what the insurer expects for an oral appliance claim under medical benefits.

For most cases, the approval packet starts with three core documents:

Those three items sound simple, but the details matter. If the sleep study is too old for the plan, if the diagnosis is not clearly stated, or if the prescription does not match the treatment being billed, the file can be delayed or denied.

The physician and dentist also document different parts of the case. The physician confirms the medical condition and orders treatment. Our office records the dental exam, scans or impressions, appliance selection, and delivery details needed to support fabrication and claim submission.

Patients are often surprised by how often small paperwork problems slow approval. A missing signature, an unreadable sleep report, or insurance information copied from an old card can add days or weeks.

Here is the checklist we ask patients to help us gather:

| Required Document | Provided By | Key Details |

|---|---|---|

| Sleep apnea diagnosis | Sleep physician | Must clearly document obstructive sleep apnea in the chart |

| Sleep study report | Sleep lab or approved home test provider | Supports diagnosis and medical need |

| Prescription for oral appliance therapy | Sleep physician | Should state that an oral appliance is prescribed for OSA treatment |

| Clinical notes | Physician office | Help explain symptoms, diagnosis, and treatment rationale |

| Appliance records | Dental office | Includes impressions or scans and treatment records for fabrication |

| Insurance information | Patient | Medical insurance details are needed for benefit verification and claim routing |

In New Jersey, another practical issue comes up often. Patients may see excellent physicians who are in network medically, but the plan may still have specific rules about how the appliance claim is submitted and what supporting records must be attached. That is why we review the paperwork before treatment moves too far. It is easier to correct a chart note early than to repair a denial later.

Bring these items together if you already have them: your medical insurance card, your sleep study report, the prescribing physician's order, and any pulmonary or sleep medicine notes you were given. One folder is best. Screenshots, partial reports, and separate portal printouts can work, but they often create extra follow-up.

If you are missing something, our team can usually tell you exactly what to request and from whom. Patients appreciate that because the process feels a lot more manageable when the next step is specific.

If an insurer still pushes back after the file is complete, it helps to understand how to contest medical insurance rejections.

Bring your medical insurance card, sleep study report, and physician prescription together. Patients who split these across multiple visits often slow their own approval timeline.

A common Fair Lawn scenario looks like this. A patient completes the sleep study, gets a prescription, and assumes the hard part is over. Then the insurance plan asks for prior approval, specific records, or a corrected diagnosis note, and the timeline slows down.

That is the point where office systems matter. At Dental Professionals of Fair Lawn, we keep the process organized so patients are not left guessing who needs to send what.

For oral appliance therapy, the steps are fairly predictable, even though each insurer applies its own rules.

Benefits are checked first

We confirm whether your medical plan covers oral appliance therapy, whether prior authorization is required, and whether there are plan-specific conditions tied to sleep apnea treatment.

The record is reviewed before submission

We look closely at the sleep study, physician diagnosis, prescription, and any supporting chart notes. Small mismatches can cause delays. A missing signature, an outdated report, or a diagnosis note that does not clearly support medical necessity can all hold up approval.

The claim is prepared with the correct medical coding

For many custom sleep apnea appliances, the code patients hear most often is HCPCS E0486. Correct coding matters, but coding alone is not enough. The claim also has to match the medical documentation on file.

Prior authorization is submitted when the plan requires it

Some plans want approval before the appliance is delivered. Others do not. We check that early, because delivering first and asking questions later can create billing problems that are hard to fix.

The final claim is sent after delivery and documentation are complete

Once the appliance is fitted and the chart supports delivery, the claim goes in for processing and payment review.

In practice, denials often come from ordinary paperwork problems, not from the appliance itself. The sleep study may be incomplete. The prescription may not match the diagnosis language. The insurer may require records from the treating physician, not just the dental office.

That is why I tell patients not to judge the process by silence. A pending claim does not always mean a problem. It often means the carrier wants one more record, one corrected form, or more time for review.

Patients also need to know that preauthorization is not the same as final payment. Prior approval helps, but the insurer can still review the claim again after delivery. That second review is one reason we document carefully from the first phone call through appliance delivery.

If a claim is denied, there is still a path to challenge the decision. This guide on how to contest medical insurance rejections explains the general appeal process and the records insurers often request during review.

Clean records, correct coding, and timely submission usually make more difference than long phone calls with the insurer.

For most patients, the practical question isn't only whether coverage exists. It's what the final bill will look like after insurance processes the claim. That answer depends on your plan's deductible, coinsurance, and whether preauthorization is required.

WebMD's review of sleep apnea treatment costs states that the average total cost for a custom sleep apnea oral appliance, including visits and adjustments, ranges from $1,800 to $2,000, and that many major medical insurance plans cover a significant portion because the appliance is categorized as durable medical equipment.

That gives patients a useful reference point. If you had no coverage at all, that general range is what you'd compare against. Once insurance applies, your actual responsibility may be much lower, but it still depends on plan design.

A few insurance terms matter more than the rest:

For Medicare beneficiaries who qualify, one common structure is 20% coinsurance after the Part B deductible, as noted earlier in the Medicare coverage discussion. Commercial plans vary more widely, which is why an exact estimate requires a benefits check.

Two things usually catch people off guard. First, "covered" doesn't always mean "free." Second, follow-up items outside the initial covered period may not be handled the same way as the original appliance.

That's why a written estimate before treatment matters. Whether you're comparing providers for sleep apnea care, restorative dentistry, Invisalign, tooth extraction, emergency dentist visits, or a cosmetic dentist near me search in Fair Lawn, financial clarity builds trust just as much as clinical skill does.

The treatment experience matters almost as much as the insurance process. Patients with sleep apnea are often already tired, frustrated, and worn down by appointments. The office experience should make things easier, not harder.

At Dental Professionals of Fair Lawn, the process starts with a consultation and record review to see whether you're already medically cleared for an oral appliance or whether a sleep physician referral still comes first. Once the medical side is in place, Dr. Jody Bardash evaluates the bite, jaw position, and overall oral health to make sure the appliance can be fitted safely and comfortably.

The office uses iTero digital scanning, which means many patients can avoid traditional goopy impressions. That makes the appointment more comfortable and creates precise digital records for the custom device.

After the appliance is fabricated, the next visit focuses on delivery and fit. The appliance is adjusted so it feels secure without being unnecessarily bulky. Follow-up visits are used to fine-tune comfort and function over time.

For patients with dental anxiety, comfort options matter too. This practice also offers sedation dentistry, which can help patients who feel tense about dental care in general, whether they're coming in for sleep apnea therapy, dental implants near me searches, cleaning and exams, cosmetic dentistry, or restorative dentistry.

A fuller overview of the process is available on the practice's sleep apnea treatment page for New Jersey patients.

A common Fair Lawn scenario looks like this: a patient finally gets diagnosed, feels relieved to have an alternative to CPAP, then gets nervous about insurance after hearing terms like denial, replacement limits, and preauthorization. Those concerns are normal. Most coverage questions can be answered once the diagnosis, device type, and plan rules are lined up correctly.

A first denial often means the insurer wants more detail, not that treatment is off the table. We see denials tied to missing records, unclear medical necessity language, or closer review of mild obstructive sleep apnea cases.

Daybreak's insurance coverage guide for sleep apnea oral devices notes that appeals can succeed, especially when the dentist sends added documentation for mild OSA cases. In practice, that usually means updating chart notes, confirming the sleep study findings, and submitting clearer support for why the appliance was prescribed.

Replacement frequency depends on the plan. Some policies allow replacement after a set number of years, while others require proof that the appliance is worn out, broken, or no longer usable.

That question is worth asking before treatment starts, especially if your medical plan has strict durable medical equipment rules or limited replacement language.

Often, no. Some plans cover the initial delivery and a limited adjustment period, then stop paying for later comfort visits or appliance modifications.

Oral appliances usually need follow-up fine-tuning, as a device can fit well on delivery day and still require small changes after a few weeks of use.

Many patients use HSA or FSA dollars for qualified out-of-pocket costs tied to sleep apnea treatment. The practical step is to save every receipt, explanation of benefits, and treatment record, then confirm eligibility with your plan administrator before you spend the funds.

Yes, it can be. Mild OSA claims tend to draw more questions from insurers, particularly if the record does not clearly show symptoms, diagnosis, and the reason an oral appliance is appropriate.

Careful charting and complete follow-up paperwork often make the difference between a delay and a cleaner approval.

Yes, and it can help. Patients sometimes get useful information about deductibles, coinsurance, and whether their plan processes oral appliances under medical benefits.

The clearer answers usually come after the office verifies benefits with the diagnosis information and the correct device coding in front of them. That is why many patients in our Fair Lawn office ask us to review the insurance details with them, then compare that information against what they heard from the carrier. It cuts down on misunderstandings and gives you a clearer picture of what to expect before the final claim is sent.

If you're looking for clear answers and a supportive path forward, Dental Professionals of Fair Lawn can help you understand your options for oral appliance therapy, review the insurance process, and schedule a consultation for sleep apnea care in Fair Lawn, NJ.